How to Start Endowments for Small to Mid-Size Nonprofits

For smaller organizations, endowments can feel overwhelming and out of reach. But while they’re often managed by universities and other large nonprofits with sizable donor pools, endowments aren’t just for wealthy organizations.

With the right strategies, support, and financial planning, small and mid-sized nonprofits can also boost their sustainability by starting endowments. In this guide, we’ll explore:

- What is an Endowment?

- Can Small Nonprofits Have an Endowment Fund?

- What is Considered a Small Endowment for Nonprofits?

- Are Endowments for Small to Mid-Size Nonprofits Worth It?

- How to Create Endowments for Small Nonprofits

What is an Endowment?

Endowments for nonprofits are dedicated, long-term funds made up of a principal donation and investment income, intended to grow over time for future use.

Traditional endowments start with a single large donation from a major donor, but organizations can also create their own board-designated quasi-endowments via a fund transfer for more flexibility. Either way, your nonprofit sets aside the original money, invests it over many years, and spends only a small percentage of the investment income each year (this is called the annual distribution).

By design, endowments are meant to be grown, not spent in full. The initial amount (the principal) typically stays intact for many years, and nonprofits only use about 4-5% of the earnings annually for mission-related purposes.

Can Small Nonprofits Have an Endowment Fund?

Yes! Nonprofits of any size can have endowment funds. All kinds of educational institutions, religious organizations, and social-service organizations use this strategy to grow their assets. These funds can be used for a range of purposes, such as:

- Supporting your general operational budget

- Providing scholarships

- Funding major projects and initiatives

- Running a specific program

One important caveat here: While any nonprofit can start an endowment, it’s a best practice to build up your reserve funds first. Endowments are not meant for emergencies or short-term funding needs, so make sure you have a healthy reserve to cover contingencies before you commit money to an endowment.

What is Considered a Small Endowment for Nonprofits?

There’s no official definition of a “small endowment,” and there are no standard minimum or maximum amounts. Nonprofit endowments can vary drastically in size, ranging from $100,000 to over $100 million. They may be even smaller, but returns will be limited.

However, a 2025 Harvard Law publication categorized small endowments as those with assets under $1 million (with the largest endowments holding over $100 million).

Are Endowments for Small to Mid-Size Nonprofits Worth It?

Every small to mid-size nonprofit has a different financial situation, so only your board of directors can determine if an endowment is worth it for your unique organization. If you’re unsure, a registered nonprofit investment advisor can help you evaluate your options and provide recommendations based on their financial expertise and experience.

In general, however, small nonprofits might consider the following pros and cons associated with endowments:

Potential Pros of Starting an Endowment

If managed responsibly, small nonprofits can benefit from maintaining endowments in a number of ways.

For instance, it sets up a long-term source of income for your organization, which can give your team peace of mind for the future and make financial planning easier due to standard annual disbursements you can consistently incorporate into your budget. Additionally, you may be able to grow your assets over time alongside your regular fundraising practices, promoting greater financial sustainability.

Nonprofit endowments can attract major donors, as well, by improving your organization’s financial reputation. Donating or contributing to your endowment also gives donors a way to stay connected with your cause and build their legacies. If their gifts are restricted, they also have more control over how those funds are spent.

Potential Cons of Starting an Endowment

As with any fundraising strategy, there are some challenges you’ll want to think through before committing to starting an endowment. In particular, small nonprofits may find that:

- Restricted funds are difficult to access and limit their ability to allocate money to the areas where they’re needed most.

- There’s an inherent risk that comes with investing funds, and they may not have the strategies to manage it.

- The cost to outsource management to a professional investment advisor is out of their budget.

- Endowments’ extended timelines may be too long for smaller nonprofits that don’t know where they’ll be in five or ten years.

Your organization can mitigate risk by establishing robust financial controls and working with a registered, fiduciary financial advisor. However, you may still determine that the potential drawbacks are not worth it for your nonprofit at this time. If that’s the case, consider focusing on your reserve funds instead!

How to Create Endowments for Small Nonprofits

If you’ve weighed the pros and cons of starting a nonprofit endowment and decided it’s the right move for your team, use these steps to get started.

1. Select a Type of Endowment

First, learn about the most common types of endowments for small to mid-size nonprofits and determine the best structure for your needs. These include:

- True endowments: Subject to many restrictions, these endowments hold the principal in perpetuity. Its earnings can only be used for specific purposes defined by donors and your endowment policies.

- Term endowments: These endowments have a specific timeframe, after which you can spend the remaining funds (including the principal) without restrictions.

- Unrestricted endowments: Many small nonprofits choose endowments with little to no restrictions, which allow them to use the funds whenever and wherever they’re needed most.

- Quasi-endowments: Created by your board of directors via a transfer of reserve funds, quasi-endowments can typically be updated or dissolved at the board’s discretion.

Small to mid-size nonprofits often choose quasi- or unrestricted endowments, since these options offer the most flexibility.

2. Get Board Buy-In

Your board is responsible for setting your organization’s strategic direction and ensuring proper fund management. Whether or not you’re creating a quasi-endowment, your board will be heavily involved in policy creation and endowment oversight, so their buy-in is essential.

Discuss options with your board of directors, and explain how a small endowment could fit into your financial strategies and drive more long-term sustainability.

3. Partner with an Advisor and Draft Policies

Next, you must craft endowment and investment policies to guide its usage. A nonprofit investment advisor can help draft these policies for you, so consider partnering with a professional at this point in the process if you haven’t already.

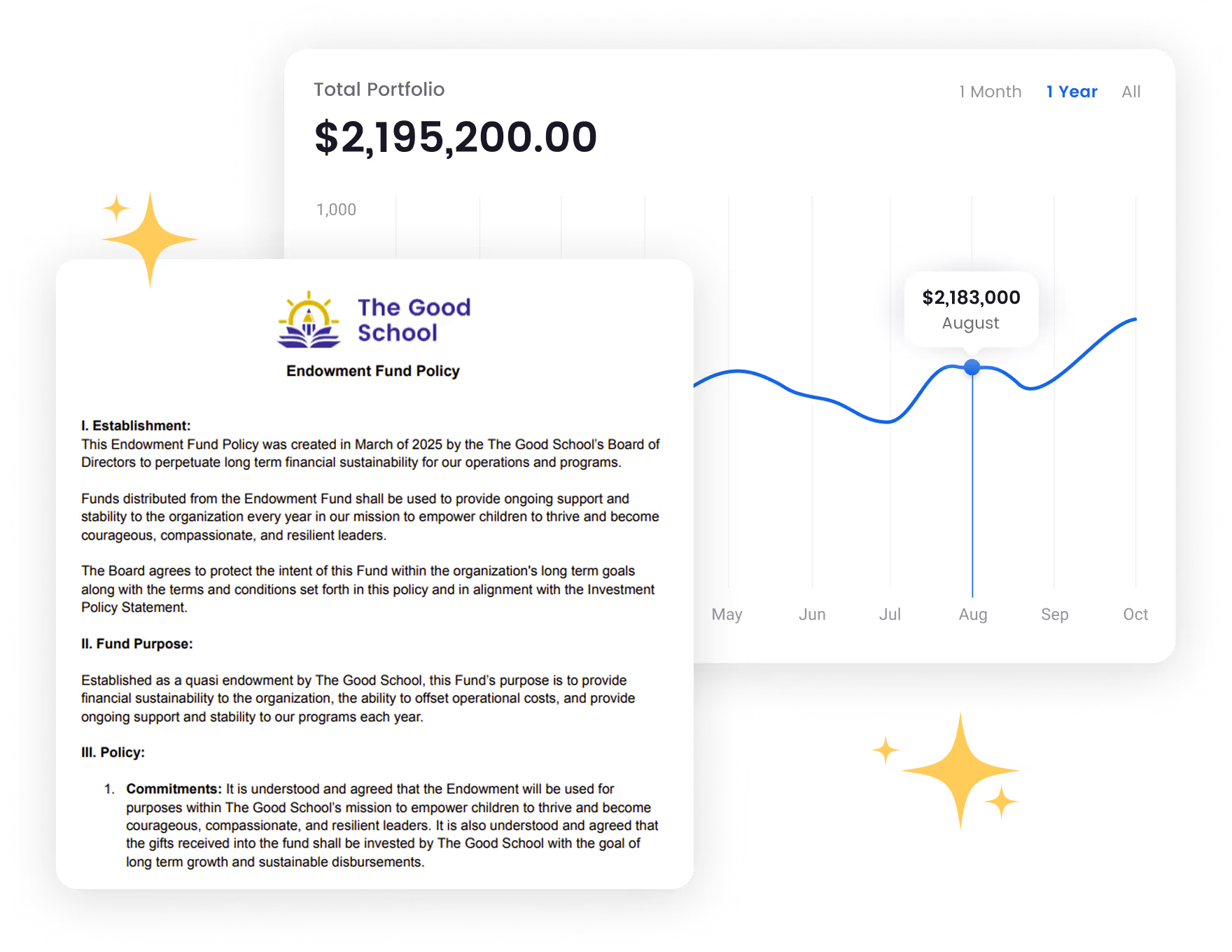

In these policies, define the endowment’s purpose, the type of endowment, what it should be used for, how it’ll be funded, and how funds will be invested, managed, and spent.

Take a look at this example of a fictional nonprofit’s endowment policies that our experts at Infinite Giving created:

If you need help developing an endowment policy that meets the needs of your small to mid-size nonprofit, book a call with our team of experts to learn how we can help.

4. Open and Fund Your Small Endowment

Finally, open your new endowment and fund it with donations (and other revenue sources, if it’s a quasi-endowment). Once established, donors can contribute to the endowment beyond the principal to build it up further.

And with the right partner, you can manage your endowment more easily by getting real-time access to a transparent financial dashboard, quarterly board reports, and secure fund transfers. Infinite Giving allows you to monitor donations to the endowment and its investment activity from one convenient dashboard. If a donor contributes a named endowment, they even get their own Donor View to monitor its growth.

Getting Support for Your Small Endowment

Small endowments don’t have to be complicated or confusing. Support from Infinite Giving’s team of nonprofit financial advisors can help you create, manage, and maintain an endowment with less hassle. Contact our team to learn more about our services and how we can help you improve your nonprofit’s financial sustainability.

For more information, check out these additional resources from the Infinite Giving blog:

- Nonprofit Endowments: Ultimate Guide to Building Your Fund. Learn more about endowments for organizations of all sizes in our ultimate guide.

- Internal Financial Controls for Nonprofits: Checklist Guide. Explore strategies and controls you can implement to mitigate financial risk at your organization.

- Nonprofit Asset Management: Basics, Benefits, & Options. Endowments are just one asset you have to manage. Discover tips for managing all your nonprofit’s assets here.

Karen Houghton, CEO and Founder of Infinite Giving

Karen Houghton is the CEO and co-founder of Infinite Giving, a Registered Investment Advisor that helps nonprofits build financial sustainability. With a background in both nonprofit leadership and venture capital, Karen brings a rare blend of heart and strategy to financial stewardship. She is passionate about democratizing access to wealth-building tools and guiding mission-driven organizations toward long-term financial health.

As a trusted advisor and advocate, Karen is reshaping how nonprofits think about money as a powerful resource for growing impact. Her work empowers tax-exempt entities to grow their assets, weather uncertainty, and fund their futures.

*DISCLOSURE

Infinite Giving Advisory Services, Inc. is an SEC registered investment adviser. Advisory services are only offered to clients or prospective clients where Infinite Giving Advisory Services, Inc. and its representatives are properly licensed or exempt from licensure. This content is solely for informational purposes. Past performance is no guarantee of future returns.

Investors’ experiences may vary from the content. Nothing in this presentation constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Infinite Giving manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary.

Individualized responses to persons that involve either the effecting of transactions in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption. Investing involves risk and possible loss of principal capital. No advice may be rendered by Infinite Giving Advisory Services, Inc. unless a client service agreement is in place. Donation services provided by Infinite Giving Technologies, Inc.

Explore More

Ultimate Guides

Articles

Grow Your Giving with Expert Nonprofit Financial Advice