Nonprofit Investing: The Ultimate Guide to Grow Your Giving

You’ve done the hard work to solicit donations, earn grants, and run successful fundraisers for your nonprofit. As a result, you’ve grown your programs and established a significant rainy-day reserve fund. Congratulations! But don’t stop there. Now that you have the funds, you must manage them strategically.

Nonprofit investing is just as important (if not more so!) as the fundraising practice itself. And it doesn't have to be high risk, either. In this guide, we’ll walk through the basics of nonprofit cash management and investing and the necessary elements to start growing your giving strategically. We’ll cover the following topics:

- Can Nonprofits Invest in Stocks?

- Benefits of Strategic Nonprofit Investing

- How to Start Investing for Your Nonprofit: 5 Steps

- Value Alignment Investing for Nonprofits

- Nonprofit Investing FAQs

When paired with valuable fundraising activities, a well-managed investment strategy can help nonprofits fund specific projects and reach long-term financial sustainability. Let’s dive in!

Can Nonprofits Invest in Stocks?

Yes! In fact, investing is strongly encouraged as part of good financial stewardship.

Many organizations invest in stocks as part of a well-rounded cash management strategy designed to generate revenue to support their mission. Nonprofits can also invest in other types of assets, such as bonds and more conservative, highly liquid strategies like Treasury Bills, Certificates of Deposit (CDs), and money market mutual funds.

The caveat is that investments cannot benefit your nonprofit’s employees or board members, per U.S. Securities and Exchange Commission (SEC) regulations. This means board members should not be managing your funds or benefiting from them in any way.

Benefits of Strategic Nonprofit Investing

The primary objective of nonprofit investing is to increase your financial sustainability. Many nonprofits have cash reserves in a simple savings account, but these funds are unlikely to be fully FDIC-insured and are actively losing value against inflation. To truly build a sustainable organization, your organization should consider how to move from a scarcity mindset to an abundance mindset by managing its cash strategically.

Just as nonprofits fundraise for different reasons, each will have specific goals for investing its reserves. Generally, the benefits of nonprofit investing fall into one of three buckets:

- Growing your reserve funds: The first step to achieving financial sustainability as an organization is saving 6-12 months of operational reserves. This serves as your emergency fund, in case a revenue stream underperforms or a pandemic happens. In this sense, you can invest for the simple goal of long-term financial stability with unused reserve funds. Generally, it’s smart to invest reserve funds in assets with high liquidity, low risk, and greatest returns.

- Cultivating large gifts: Major donors may look to your assets to confirm your financial stability before donating. A healthy reserve fund invested wisely (especially one that readily accepts endowment and stock donations) can encourage large gifts by demonstrating how your nonprofit plans to use donations strategically for many years to come.

- Building long-term assets: Especially if you don’t own much capital, funding a conservative investment portfolio can bolster your balance sheet and reputation while increasing buying power and impact.

Ultimately, your investment goals will depend on factors like your timeline, current assets, and regular fundraising behavior. They should also be guided by a sound Investment Policy Statement (IPS), which a Nonprofit Investment Advisor should create for you at no extra cost. Plan to address these goals in routine conversations with key stakeholders, your board of directors, and your Nonprofit Investment Advisor.

How to Start Investing for Your Nonprofit: 5 Steps

Ready to start an investment account? Let’s walk step-by-step through what it takes to invest in your nonprofit.

1. Choose a Nonprofit Investing Partner

Investment resources have been historically inaccessible for nonprofits, particularly for small to mid-sized organizations. The high minimums and advisory fees associated with big banks and brokers are often a deterrent, and DIY investing is risky. That’s why it’s crucial to choose an outside partner who can help manage your portfolio effectively and take on a consistent fiduciary role.

We highly recommend you consider working with a specialized nonprofit advisor who offers both financial expertise and insight into the unique challenges nonprofits face. That said, there are several types of partners you can work with:

Big Banks

For nonprofits of any size, big banks can offer a traditional investing experience. However, “traditional” isn’t always best. When deciding if a big bank is right for your nonprofit investing, consider that big banks:

- Don't typically have nonprofit expertise.

- Don't typically offer the best rates available.

- Require high fees to cover their overhead.

- Often have high minimums and aren't open to smaller nonprofit investments (under $10 million).

- Require extensive paperwork.

- Have long timelines to get things done.

- Put a middleman between you and your money.

- Can make fund transparency and access difficult.

- Lack an integrated technology platform.

Wealth Advisors and Brokers

Traditional brokers and wealth advisors offer another avenue for nonprofits looking for a typical investing experience. However, brokers are not fiduciaries—meaning that they can promote their own interests or the interests of companies when it comes to your investments.

When deciding if a traditional advisor is suitable for your nonprofit, consider that this option:

- Requires choosing a wealth advisor, which can become highly political and messy due to nonprofit board relationships.

- Involves long timelines and extensive paperwork to get things done.

- Usually has high fees (generally 1% or higher).

- Puts a middleman between you and your money.

- Can make fund transparency and access difficult.

DIY

While you can invest directly through Fidelity or Schwab, it's not considered a best practice for several crucial reasons. The clear positive is it cuts down on fees, but these banks still have high minimums, and it also comes with great fiduciary responsibilities for nonprofits.

Volunteer board members who do this often have the best of intentions, but they’re still volunteers, meaning you end up with a lack of oversight, accountability, and transparency in DIY investing. There's typically a loss of consistency when board member terms are up or two professionals have differing opinions. It also opens up your organization to scrutiny from donors and relational fallout if mistakes are made.

Keep in mind that DIY investing:

- Can reduce advisory fees but can also be confusing and hard to understand.

- Gives you sole fiduciary responsibilities.

- May not offer you the reporting or performance metrics you need.

- Might involve potential conflicts of interest.

- Lacks consistent oversight as a result of limited board terms.

- Lacks a plan for addressing underperforming funds.

- Requires extensive expertise, time, and interest to take on creating and rebalancing the portfolio.

Nonprofit Investment Advisors

Nonprofit Investment Advisors take on fiduciary responsibilities and partner with nonprofit organizations as outsourced Chief Investment Officers (CIOs), meaning they’re required to work in your organization’s best interest.

Due to nonprofits' reduced capacity for risk, Nonprofit Investment Advisors recommend a variety of portfolios, from mutual funds, CDs, and Treasury Bills to securities and bonds. They also often leverage Index Investing to bring you the greatest returns possible within the risk category you are most comfortable with.

Today, Infinite Giving is one of the only firms created specifically to serve small to mid-size nonprofits. We leverage technology, financial expertise, and decades of nonprofit experience to reduce overhead and bring nonprofits a modern investing and giving experience. Our Nonprofit Investment Advisors:

- Have decades of experience in nonprofit finance.

- Provide consistent fiduciary oversight.

- Prioritize low-risk, highly liquid investments.

- Aim to build your nonprofit’s wealth gradually over time and mirror the market.

- Have reduced and transparent fees.

- Provide easy tools to grow asset giving.

- Offer quarterly board reports.

- Bring high transparency and easy access to funds.

- Have a low minimum requirement.

- Offer an intuitive platform that tracks all your investment activity in one place.

As you decide who to partner with to invest your funds, keep in mind that an Investment Advisor is the only option that serves as a true fiduciary for your nonprofit. They also typically offer much lower fees than big banks or brokers.

2. Develop a Nonprofit Investment Policy Statement

Before you invest, establish clear governance policies that address your investment account strategies and management policies. Nonprofits collect these policies in a document called a nonprofit investment policy statement (IPS), which is a roadmap for how an organization wants to invest its money. An IPS provides your Investment Advisor, board of directors, and team with guardrails for financial stewardship for your nonprofit.

Your IPS should be a simple document that can be passed to new board members as legacy members leave. You also should not need to pay an attorney to create these documents. A good Nonprofit Investment Advisor will help you work through one at no cost, and you can use templates like the one below to rework and edit as needed.

Your policy statement should include the following details:

- Roles of Investment Committee. Summarize the roles, responsibilities, and limitations of stakeholders (e.g., Board of Directors, Oversight Committee, and Executive Director) accountable for overseeing and managing a nonprofit’s investment portfolio.

- Investment Objectives. Define the primary goals for the investment portfolio, the long-term target rate of return, and the potential risk allowed.

- Investment Policies. List the types of investments allowed/prohibited and the target percentages of funds allocated to each type.

- Performance Measurements and Reporting Standards. Outline the standards and frequency by which the Board of Directors will measure and report on fund performance.

- Spending Policies. State all uses, benefits, purposes, and factors relevant to spending the nonprofit’s investment funds. Include guidelines for how, why, and when funds can be added to, withdrawn from, and reallocated in the investment account.

- Donor Restrictions. Clearly state that the investment committee agrees to all stipulations made by donors for how their funds are used and invested.

To make your life easier, download our free investment policy statement template to create your governance policies. However, resist the urge to fill this out and never think about it again. Your investment policy statement should be a living document that operates in conjunction with your strategic plan, bylaws, and statement of activities. Alongside your Board of Directors and your Registered Investment Advisor, continue to revise these statements as your nonprofit's needs and circumstances change.

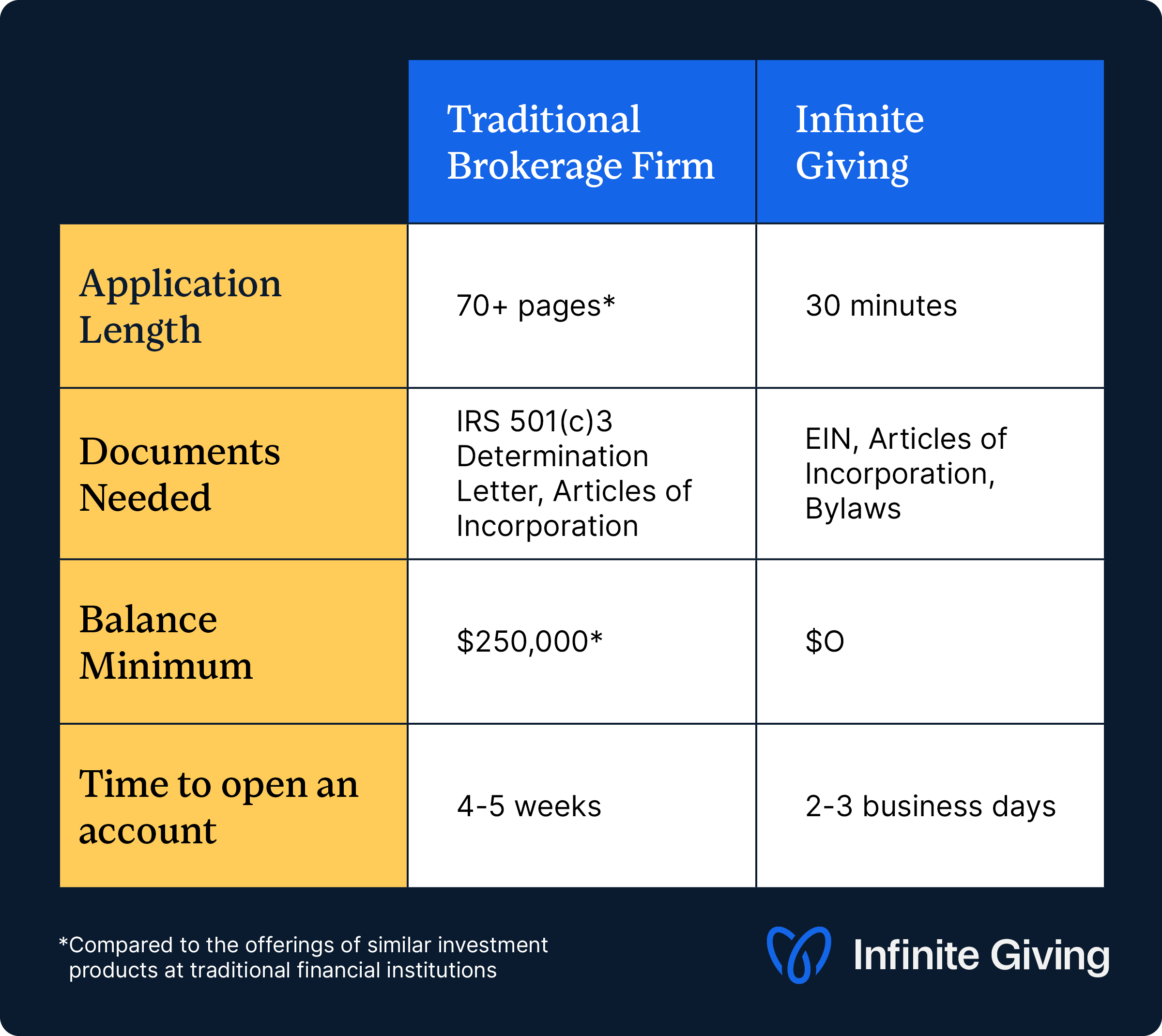

3. Open a Nonprofit Investment Account

Once you’ve decided on your investment account solution, you’ll then open your account. To do so, you’ll need the following documents to prove your nonprofit status:

- An account application (with basic nonprofit information like your EIN and contact details)

- A copy of your Articles of Incorporation

- A copy of your 501(c)(3) IRS Determination Letter

- A copy of your organization’s bylaws

Gather these documents ahead of time so you can get up and running quickly. Depending on the method you use and who you choose to partner with, the application process can be completed in minutes or take weeks. For example, take a look at the differences between applying for a traditional brokerage account and an investment account with Infinite Giving:

4. Outline Your Nonprofit Investment Strategies

The type of account you have and the strategies you use greatly impact the success and accessibility of your investments.

Most nonprofits prioritize low-risk, highly liquid investment strategies. These types of assets, such as treasury bills, short-term CDs, and money market accounts, provide stability and ease of access if funds are needed unexpectedly. As you choose your strategies, consider the pros and cons of each one:

Money Markets and Savings Accounts

While money market accounts and savings accounts are often considered a relatively “safe” form of investment, the returns they generate are so low that your funds may be actively losing value due to inflation.

Funds that are held in savings accounts also run into FDIC insurance limits of $250,000. Bank failures do happen, so you want to limit your risk of holding over $250,000 per bank outside of your typical operating budget.

When considering money market and savings accounts, remember that these funds:

- Are typically not FDIC-insured beyond $250,000.

- Offer high liquidity.

- Often require minimum balances with your bank.

- Generate some income, but little capital appreciation.

- Are not suitable as long-term investments.

- Could likely lose value over time due to inflation.

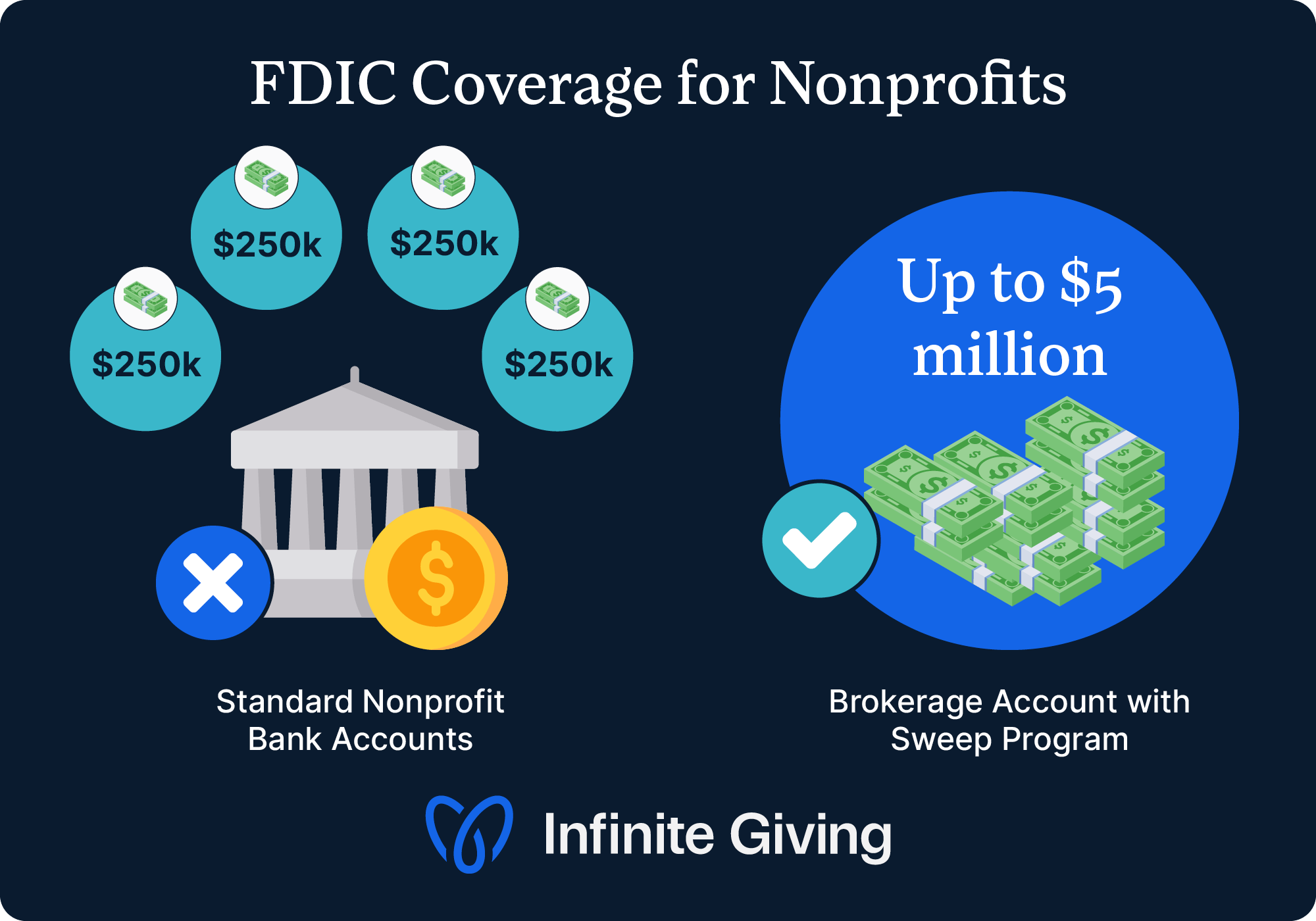

FDIC Sweep Accounts

One of the easiest ways to lower your banking risk is to diversify into a brokerage account with a sweep program that increases your FDIC coverage. This way, you can keep all your reserve funds in one account and ensure that all of your funding is insured.

For example, Infinite Giving’s sweep accounts offer up to $5 million in FDIC coverage from one streamlined account.

Compared to keeping multiple smaller accounts at separate institutions, this is a much more efficient way to manage and invest your organization’s reserve funds.

CDs and CDARs

While CDs, mutual funds, and money markets are all low-risk cash reserve management options for nonprofits, CDs tend to be less flexible and less liquid. Additionally, they’re also subject to the FDIC insurance cap of $250,000 per financial institution.

If your nonprofit chooses to purchase CDs with more than $250,000, we strongly suggest using a Certificate of Deposit Account Registry Service (CDARS) program so that all funds remain FDIC-insured. This program helps nonprofits easily distribute their investments across banks and accounts to get more than $250,000 in total FDIC coverage without having to manage everything manually. Working with a nonprofit investment advisor like Infinite Giving makes the process easy.

Treasury Bills

Treasuries are currently a popular opportunity for more risk-averse organizations that still want targeted growth.

Your Nonprofit Investment Advisor can buy a treasury bill at a set price and let it mature at a fixed rate of interest over the course of a few months (or years if you buy a treasury bond). Typically, these are rolling portfolios that are automatically repurchased at the end of each yield. At the end of the maturity period or whenever you withdraw the funds, your nonprofit gets paid for the face value of the bill at that time.

If needed, Investment Advisors can also sell treasury bills for you on secondary markets in between yields. This way, the funds remain highly liquid, and you can typically access the cash in 3 business days.

5. Monitor Results & Boost Fundraising Capabilities

With your account and strategies solidified, the next step is to fund your account with cash reserves and leverage it to raise additional funds. Keep track of your investing activity and yields by getting regular reports from your portfolio manager.

As you put your reserve funds to work, make sure to optimize and build up other revenue sources, too. Having an investment account can allow your nonprofit to accept and manage new types of donations easily, including:

To simplify accepting these non-traditional donations, partner with a provider that offers streamlined, intuitive non-cash donation pages. Infinite Giving makes it easy for you to accept these donations and for donors to initiate a transfer right from your donation page.

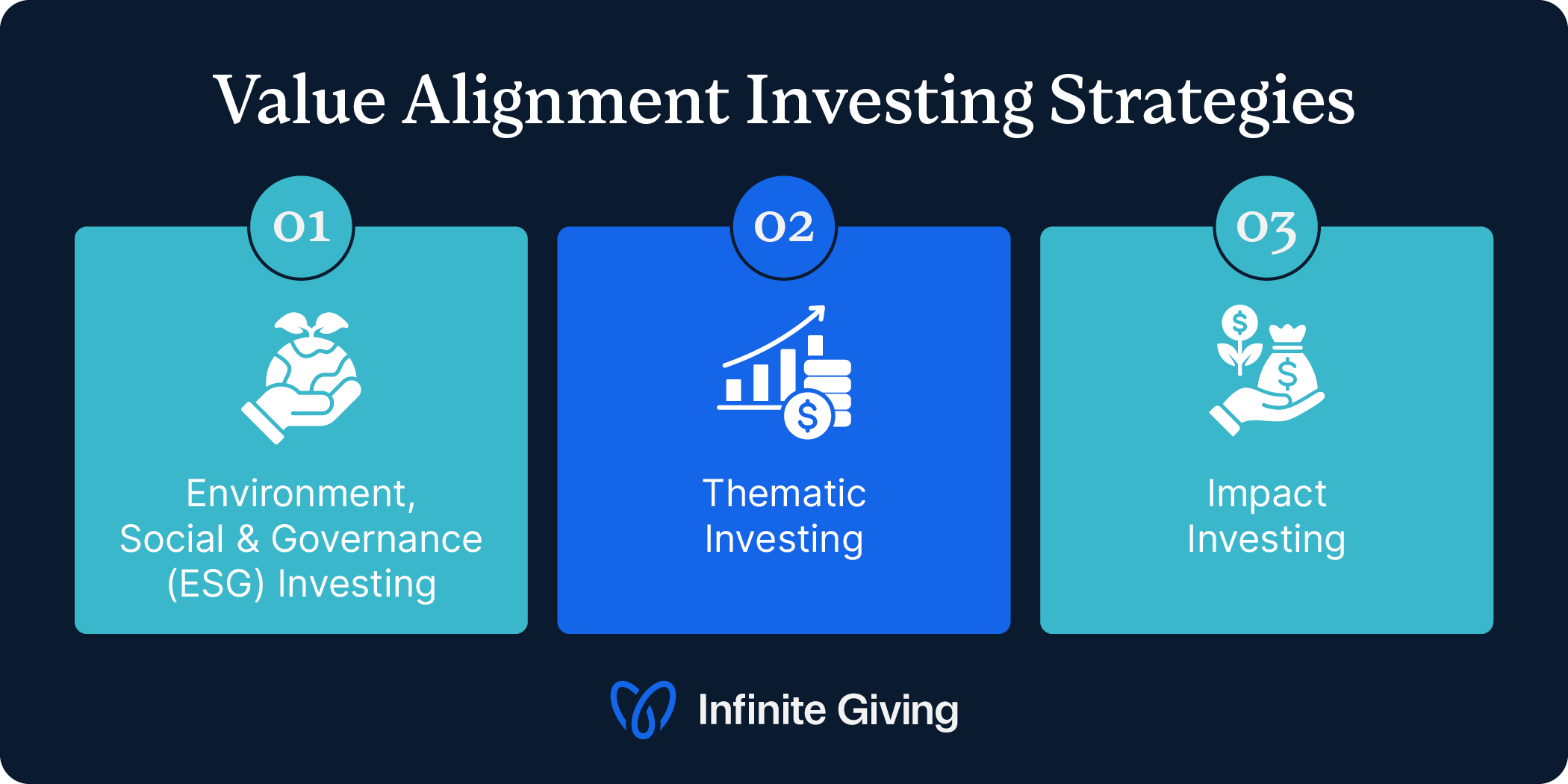

Value Alignment Investing for Nonprofits

Contrary to popular belief, there isn’t a single right way to invest your nonprofit’s money. Nonprofits can invest according to a range of strategies. Only you can determine which one is the right approach for your nonprofit.

In most cases, you want a strategy that protects the value of, grows, and allows you to access your assets. However, for those committed to a focused mission, you’ll likely also want a strategy that considers additional factors about where you invest your funds.

Let’s walk through the process of evaluating different nonprofit investment strategies and why they may be a good fit for your nonprofit. These include:

- Environment, Social, and Governance (ESG) Investing. This takes a step beyond value alignment to actively search out companies that align with the core ethics of environmental, social, and governance criteria. Environmental investing considers a company’s conservation practices, carbon footprint, pollution, and use of renewable energy. Social investing considers how a company treats its employees and customers, workforce diversity, labor conditions, and community involvement. Governance investing considers how a company is run, its shareholder treatment, the diversity of its board, the transparency in its accounting, and its political influence.

- Thematic Investing. This investing strategy allows investors to focus their investments on a specific theme or industry, such as faith-based organizations or companies with women in leadership. For example, a nonprofit committed to environmental justice might thematically invest in companies in the renewable energy industry.

- Impact Investing. This strategy focuses not on financial return but on making the largest measurable social or environmental impact. Generally, these investments are not available in the public market and are relatively illiquid.

Luckily, you don’t have to choose between sacrificing your values and growing your funds. A 2020 report from Morgan Stanley found that sustainable fund portfolios outperformed traditional funds.

No matter where you invest your money, remember to consider your timeline, other sources of revenue, and risk tolerance. Generally, a longer timeline (e.g., investing for long-term savings) and more consistent cash flow (from recurring unrestricted gifts and grants) can open up additional investment for longer-term, higher risk, and less liquid opportunities.

Nonprofit Investing FAQs

Many people have misconceptions and misunderstandings about the nonprofit investing process, so let’s take a quick look at nonprofits’ biggest investing questions.

Can Nonprofits Invest?

Yes! Investing is strongly encouraged as part of good financial stewardship. Nonprofits can invest in various financial instruments, including stocks, treasury bills, and certificates of deposit (CDs). Given that nonprofits typically have a lower risk tolerance, they often focus on low-risk assets like treasury bills, which can be liquidated easily if necessary.

What Types of Funds Do Nonprofits Invest?

Commonly, nonprofits invest reserve funds and endowments. Capital campaign funds and grants can also be placed in low-risk sweep accounts. Investing reserve funds (your "rainy day fund") can help combat inflation, preserving their value over time. Endowments are another key resource, as they’re meant to be invested for long-term growth.

Can a Nonprofit Have an Investment Account?

Yes, nonprofits can have investment accounts, also known as brokerage accounts. In fact, as a part of good financial stewardship, you should highly consider having one.

As a registered 501(c)(3) organization, you are generally exempt from paying federal income tax on investment portfolio dividends and gains. Thus, a nonprofit’s investment account has built-in, money-saving value over those of for-profit businesses. Your tax-exempt status can help to increase your overall return potential and allows you to change investments without significant tax implications.

Investment accounts can be used for low-risk, highly liquid strategies such as Treasury Bills and money market mutual funds, in addition to growth and endowment-oriented accounts that include Index Funds and Bonds. Brokerage accounts are also used to receive stock donations, which can grow high-capacity giving.

Can Nonprofits Buy Treasury Bills?

For a low-risk investment choice or in addition to investing in stocks, nonprofits can buy treasury bills or treasury bonds. These are some of the lowest-risk investments you can make because they’re fully backed by the US government if held to maturity. Treasury bills are rising in popularity for nonprofit reserves due to rising yield rates that are highly liquid and often bring greater returns than money markets and savings.

Can a Nonprofit Invest in CDs?

Like other traditional investment options, nonprofits can invest in Certificates of Deposit (CDs) if they choose to do so. CDs are bank securities that remain at a fixed interest rate for a specific period. For instance, you might buy a CD with an interest rate of 3% and a maturity period of three years. In this case, your organization can only earn 3% interest and cannot access the funds for three years without penalty.

Can Nonprofits Receive Mutual Funds?

The answer to this question depends on your provider. Not every non-cash donation tool allows you to accept mutual funds, but Infinite Giving does. With our all-inclusive asset donation page, your organization can easily accept gifts of cash, stocks, mutual funds, crypto, and DAF grants.

What Does Your Nonprofit Need to Start Investing?

Your organization will need:

- A brokerage account

- A well-defined Investment Policy Statement (IPS)

- A trusted partner, such as an investment advisor

While it’s possible to manage investments independently through a firm like Fidelity or Schwab, working with a specialized Nonprofit Investment Advisor can make the process smoother, less risky, and more effective.

How Do You Choose an Investment Advisor?

You (hopefully) wouldn’t hand your wallet over to just anyone. As in any business partnership, you need to trust the person or entity holding your money and know they’d do their best to grow your investment. Similarly, now is the time to be selective with where you invest your nonprofit’s funds.

Consider choosing a Registered Investment Advisor (RIA) who meets SEC compliance requirements to mitigate risk. Unlike other types of financial advisors, such as broker-dealers, RIAs have a fiduciary obligation to act in your nonprofit’s best interest and offer you the lowest-cost products that meet your needs.

We also recommend finding an Investment Advisor who works exclusively with nonprofits. Your needs as an NPO vary greatly from personal or for-profit investment strategies, so having an expert who can speak to industry standards and make recommendations on policies, procedures, and investment strategies is incredibly valuable.

How Much Money Does a Typical Nonprofit Have to Invest?

There’s no standard amount of funds a nonprofit has to invest, as this depends on individual financial situations and investment goals.

Ideally, experts recommend keeping six to 12 months’ worth of your organization’s operating costs in reserve, and as we mentioned earlier, it’s worth considering placing your reserve funds in investment vehicles to avoid them losing value in a savings account. However, this isn’t feasible for many nonprofits, and anything is better than nothing. As you gain more financial sustainability, you can aim to invest 12 months to two years’ worth of operating costs.

You may need to set aside a certain amount of funding to open a brokerage or investment account. This amount varies depending on the brokerage firm or investment solution, so be sure to research any requirements ahead of time to prepare.

Additional Resources

Want to learn more about investing for your nonprofit? Explore the following tools and resources:

- Nonprofit Brokerage Accounts: Guide, FAQ, & How to Open One. Dive deeper into the steps to opening a nonprofit investing account, along with your options for doing so.

- Cash Management for Nonprofit Organizations: Basics + 8 Tips. Nonprofit investing is a crucial part of effective cash management. Check out this resource to learn more about managing your cash strategically.

- Nonprofit Reserve Funds: How to Manage Operating Reserves. Interested in sustainable nonprofit development? Learn about why and how your nonprofit should prioritize growing your reserves.

*DISCLOSURE

Infinite Giving Advisory Services, Inc. is a registered investment adviser in the States of Georgia, California, Colorado, North Carolina, Pennsylvania, and Texas. Advisory services are only offered to clients or prospective clients where Infinite Giving Advisory Services, Inc. and its representatives are properly licensed or exempt from licensure. Our firm may not transact business in states where it is not appropriately registered, excluded or exempted from registration. This content is solely for informational purposes. Past performance is no guarantee of future returns.

Investors’ experiences may vary from the content. Nothing in this presentation constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Infinite Giving manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary.

Individualized responses to persons that involve either the effecting of transactions in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption. Investing involves risk and possible loss of principal capital. No advice may be rendered by Infinite Giving Advisory Services, Inc. unless a client service agreement is in place. Donation services provided by Infinite Giving Technologies, Inc.

Explore More

Ultimate Guides

Articles

Grow Your Giving with Expert Nonprofit Financial Advice