Nonprofit Reserve Funds: How to Manage Operating Reserves

It’s natural that many nonprofits are so focused on making a positive impact on their communities that they neglect financial stewardship in favor of fundraising. However, your organization can't just raise money—you also have to manage it effectively.

Stewarding your nonprofit’s finances is crucial to its long-term success. To increase your financial sustainability and be prepared for the unexpected, your nonprofit needs a reserve fund. In this guide, we’ll help you become more financially secure by covering:

- What Are Nonprofit Reserve Funds?

- Types of Nonprofit Reserve Funds

- How Much Money Should a Nonprofit Have in Reserve?

- How to Create a Nonprofit Reserve Fund Policy

- Best Practices for Managing Your Operating Reserves

Building a reserve fund is only the beginning. With proper stewardship and cash reserve management, your nonprofit can grow its operating reserves and ultimately achieve more for your mission.

What Are Nonprofit Reserve Funds?

A nonprofit reserve fund, also called cash reserves or a rainy day fund, is a nonprofit organization’s version of a savings account. Unlike funds allocated toward daily programs or activities, these are unrestricted funds set aside from normal operating funds and used sparingly.

Generally, cash reserves are meant for emergencies when expected income falls through or when unexpected expenses hit. Developing a healthy reserve fund should be one of your first financial priorities. In doing so, you’ll build a sound, sustainable organization that progresses beyond a scarcity mindset.

Can Nonprofits Have Reserve Funds?

Not only are nonprofits allowed to have reserve funds, but for their long-term financial health, they should have reserve funds. Reserve funds are a key financial piece of the puzzle as a nonprofit seeks financial resiliency and builds capacity over time.

Where Do Nonprofit Operating Reserves Come From?

For nonprofits, reserve funds can come from a number of different sources. They may be set aside from a surplus at the end of a fiscal year, given from a donor, or accrued from a line in your operating budget.

Additionally, nonprofits can actively grow and replenish their existing reserve funds by taking proactive steps like:

- Identifying reserve growth as a component of a capital campaign.

- Allocating portions of grants or sales proceeds to the reserve fund.

- Investing existing reserve funds.

- Delaying new short-term programs to build long-term sustainability first.

In any case, just like you would build a savings account for your personal household, you should make intentional plans for where you fund and maintain your cash reserves.

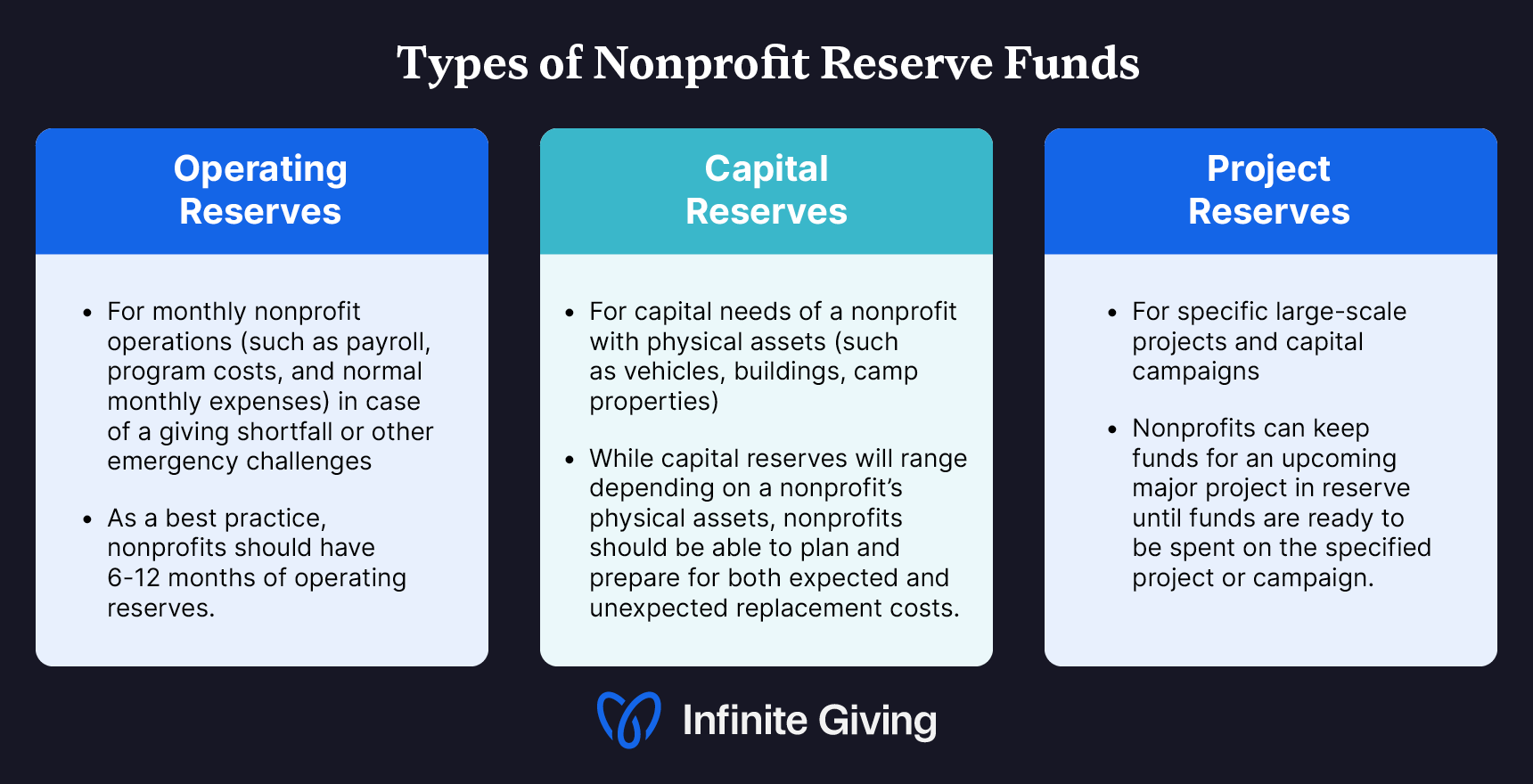

Types of Nonprofit Reserve Funds

Many small and medium-sized nonprofits might end up with just one reserve fund for all their activities. However, we advocate for separate funds for optimal tracking, budgeting, and transparency. You’ll distinguish these based on their amounts, timelines, and intended uses.

When building your nonprofit’s reserve fund, there are three main types you might need:

Operating Reserves

Operating reserves are funds intended to keep a nonprofit’s monthly operations going (think overhead like payroll, program costs, and normal monthly expenses) in case of a giving shortfall or other emergency challenges.

For example, with today's steep rise in inflation, nonprofits with a healthy operating reserve fund are better positioned to adapt to increased prices for labor and goods—without putting themselves at risk.

As a best practice, nonprofits should set aside enough operating reserves to fund 6-12 months of regular operations. If a nonprofit can save enough money to meet its operating needs for more than twelve months, those additional funds can be used to start new programs or to seed an endowment and establish further organizational sustainability.

Capital Reserves

Capital reserve funds are funds that are saved and set aside for the capital needs of a nonprofit with physical assets, such as vehicles, buildings, and camp properties.

By owning or leasing physical property and assets, you should expect to incur capital expenses such as repairs and replacements of often large and expensive items. After all, roofs need replacing, engines need maintenance, and weather events happen.

The amount of capital reserves you need will depend on your physical assets. Assess your unique needs and plan for both expected and unexpected replacement costs. This strategic financial stewardship brings stability and decreases stress on both your organization and your donors.

Project Reserves

Lastly, some nonprofits keep project or campaign reserves if they’re preparing for a major project they’re not yet ready to launch. For instance, you might need a project reserve fund if you’re planning a capital campaign that won’t begin for another two years.

There’s no set amount you need to keep in project reserves—it depends on how much funding you want to set aside now for the specified future project. Any early donations you receive can be kept here until the funds are ready to be spent on your major project or campaign.

How Much Money Should a Nonprofit Have in Reserve?

As you may have guessed, different nonprofits will need to set different goals based on their financial situation.

In general, however, we recommend that you keep 6-12 months’ worth of your nonprofit’s operating costs in reserve.

For nonprofits with less than six months of cash reserves, these goals may seem out of reach. If this is you, don’t give up! Start by intentionally creating strategies to build your reserves, and make sure you place them with a Nonprofit Investment Advisor who can ensure they are FDIC-insured and placed in low-risk, highly liquid holdings. Giving yourself a solid foundation to build upon is the first step to cultivating financial sustainability.

Where to Keep Nonprofit Reserve Funds

While your first instinct may be to store your nonprofit’s entire reserve fund in a checking or savings account, this isn’t the way to go. Keeping your nonprofit reserve funds in traditional bank accounts can put your funding at risk and limit its growth opportunities.

Instead, you should keep your cash reserves in:

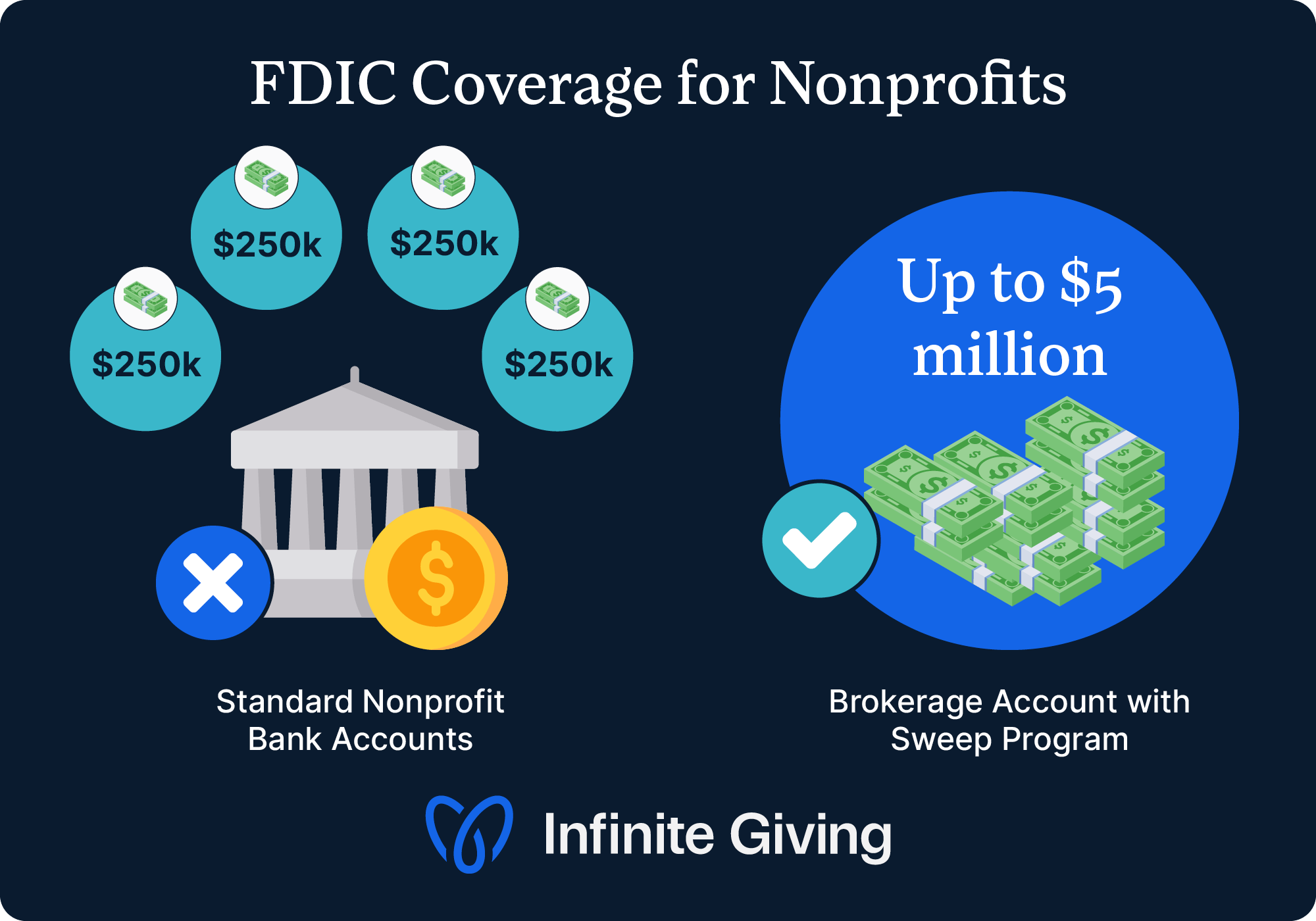

FDIC-Insured Accounts

It's incredibly important to ensure your reserve funds are FDIC-insured. Banks can fail, and it's your organization’s responsibility to ensure that your donations are protected by the government if that happens.

Make sure you have FDIC coverage for all of your funding by keeping your reserve funds in the right type of account. Let’s explore what FDIC coverage looks like for traditional bank accounts vs. brokerage accounts:

- Most banks offer nonprofits FDIC coverage only up to $250,000 across all types of accounts. This means that if you have more than $250,000 in your reserve fund, it’s not all covered. To maintain FDIC coverage for all of your funds, you must open and manage multiple different accounts with less than $250,000 in each.

- Brokerage accounts with sweep programs let you access FDIC coverage for up to $5 million in one account. This means you’ll have only one account to keep track of, simplifying bookkeeping and making it easier to access and manage your funds.

By choosing an Infinite Giving brokerage account to store your reserve funds, you’ll get FDIC coverage up to $5 million on cash reserves, with no minimums. Save your organization time, stress, and effort by managing everything from one secure account.

Nonprofit Brokerage Accounts

Keeping your reserve funds in a brokerage account with a sweep program not only gives you more FDIC coverage, but it also allows you to:

- Invest your reserve funds in low-risk, highly liquid holdings to help them grow over time.

- Accept and process stock donations, boosting your nonprofit’s fundraising capacity and ability to engage donors.

- Achieve financial sustainability by managing all your reserve funds in one place, making strategic investments, and soliciting stock donations.

While you can access some of these benefits from traditional brokerage firms like Fidelity and Schwab, we recommend choosing a Nonprofit Investment Advisor instead. Opening a brokerage account with nonprofit specialists like Infinite Giving gives you access to expert advice and years of nonprofit experience to get you up and running faster.

Low-Risk Investments

Once you have a brokerage account and sufficient FDIC coverage, start stewarding your reserve funds by investing them in a range of places to maximize their value and usefulness.

Nonprofit reserve funds need high liquidity and easy access for short-term needs, but they also need to have capital preservation for their longer-term needs. Thus, as a best practice, most nonprofits should plan to invest their reserve funds in conservative, liquid holdings such as money market mutual funds, Treasury Bills, and CDs to retain buying power over the long term.

When deciding how and where you’ll place your cash reserve funds, consider asking the following questions of each provider:

- What are the current rates and yields for their conservative offerings?

- Will your funds be FDIC-insured?

- Can they help you create an Investment Policy Statement?

- How will you access your funds when needed? Are there penalties?

- What types of security features does the provider offer?

- How easy is it to work with the provider and use their investment platform and services?

Infinite Giving can help you create multiple FDIC-insured reserve accounts that are conservatively invested and often bring higher returns than banks. Our nonprofit experts partner with nonprofit teams and their boards to help you manage your cash reserves, create endowments, and even receive donations through our donation platform. Plus, you have complete access to your funds at any time and can easily transfer from your reserves to your checking account as needed.

How to Create a Nonprofit Reserve Fund Policy

Without clear policies, reserve funds can easily be spent and depleted over time, putting nonprofits at undue financial risk. Before you start building your nonprofit cash reserve fund, develop an accompanying reserve fund policy statement to guide the fund’s management. Your policies should address strategies, spending policies, cash thresholds, key stakeholders, and asset allocation.

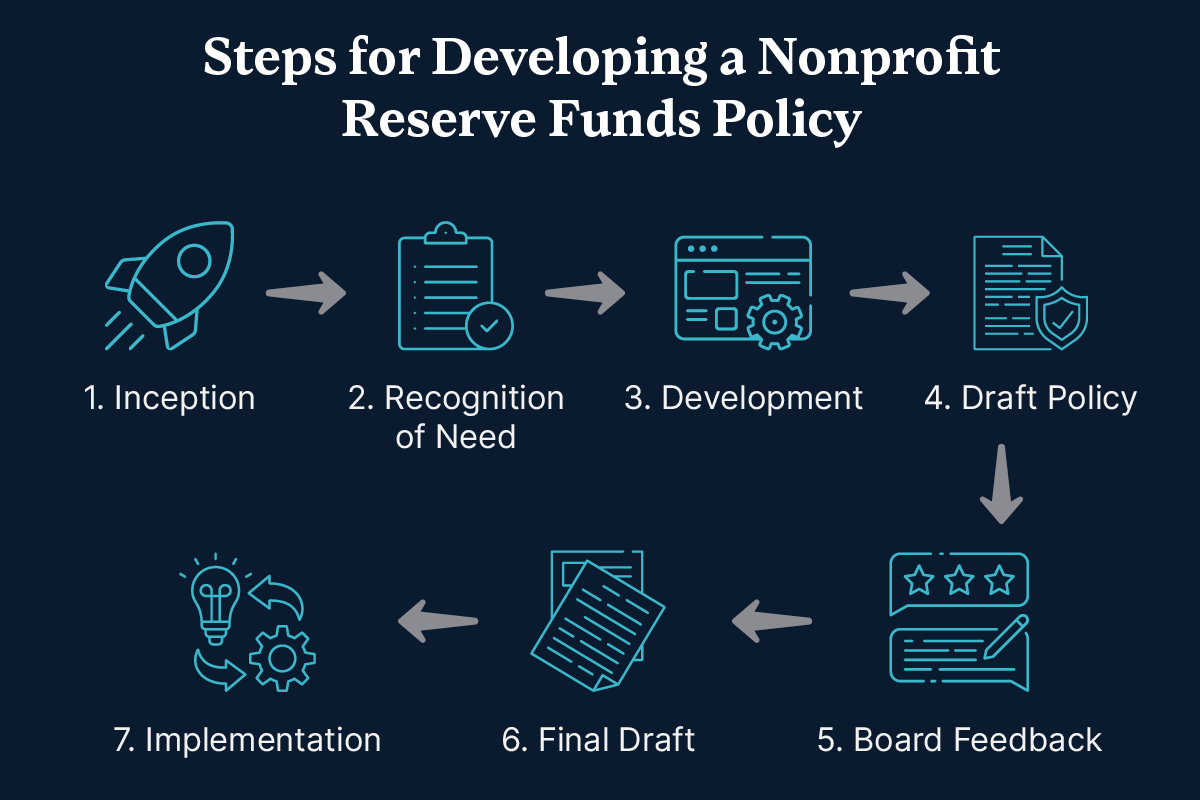

When you work with a Nonprofit Investment Advisor, they should create this policy for you at no additional cost. Typically, the policy creation process involves these key steps:

- Inception. Begin a conversation with key stakeholders, including board members, about the need for a reserve fund policy.

- Recognition of Need. Stakeholders (hopefully) will acknowledge the need for a reserve funds policy and offer their initial thoughts.

- Development. Once you’ve secured buy-in, work with your team or a related committee to conduct initial research.

- Draft Policy. Your Nonprofit Investment Advisor will draft a policy that includes sections for both cash management and investments.

- Board Feedback. Present the policy to key stakeholders for their feedback. Stakeholders may request revisions and edits.

- Final Draft. Incorporate feedback, finalize the policy statement, and submit it to your board for approval.

- Implementation. Put your policy into practice as you begin building your nonprofit reserve fund!

Explore our free investment policy statement template to see what one of these policies looks like in action. If you have questions about creating a policy that meets your organization’s unique needs, discuss them with your Nonprofit Investment Advisor before they begin the policy creation process.

Best Practices for Managing Your Operating Reserves

To give you a strong starting point for reaching your reserve fund goals, we’ve compiled a list of recommended best practices that will put you in the best position for success.

A nonprofit in a strong financial situation should practice the following strategies:

- Make your operating budget easily accessible by placing it in a checking account or high-yield savings account and not considering part of your reserves.

- Partner with a Nonprofit Investment Advisor to access more FDIC coverage through a sweep program.

- Separate reserves outside of the nonprofit’s annual budget. These true cash reserves should be clearly marked for planning purposes.

- Place operational and capital reserves in low-risk, highly liquid investment strategies such as money market mutual funds or Treasury Bills.

- Use additional funds to conquer other goals such as starting new ventures, creating a growth portfolio, or seeding a quasi-endowment for long-term sustainability.

If all of these steps are feasible for your nonprofit, you’re in an excellent position to grow both your financial portfolio and your community impact.

Additional Resources

Ready to dive further into cash reserve management and grow your nonprofit reserve funds? Take a look at our additional guides:

- Nonprofit Brokerage Accounts: Guide, FAQ, & How to Open One. Learn more about the benefits of keeping your reserve funds in a brokerage account with more FDIC coverage.

- How to Accept Stock Donations: The Ultimate Nonprofit Guide. Many nonprofits don’t realize the benefits of stock (and crypto!) donations. Learn how accepting large asset gifts from high-capacity donors can help grow your reserve funds.

- Nonprofit Investing: The Ultimate Guide to Grow Your Giving. Wade into the world of nonprofit cash management and investing with this comprehensive guide.

Karen Houghton, CEO and Founder of Infinite Giving

Karen Houghton is the CEO and co-founder of Infinite Giving, a Registered Investment Advisor that helps nonprofits build financial sustainability. With a background in both nonprofit leadership and venture capital, Karen brings a rare blend of heart and strategy to financial stewardship. She is passionate about democratizing access to wealth-building tools and guiding mission-driven organizations toward long-term financial health.

As a trusted advisor and advocate, Karen is reshaping how nonprofits think about money as a powerful resource for growing impact. Her work empowers tax-exempt entities to grow their assets, weather uncertainty, and fund their futures.

Explore More

Ultimate Guides

Articles

.jpg)

Grow Your Giving with Expert Nonprofit Financial Advice